Southeast Asia’s deep tech sector is carving out a larger share of the region’s venture ecosystem, even as deal activity slows, with rising funding value pointing to fewer, larger and more selective bets, according to DealStreetAsia’s Southeast Asia Deep Tech Review: 2025.

In a sign of the tough fundraising environment, deep tech funding softened in 2025, with deal volume falling to 109 from 117 in 2024. Yet the pullback in activity did not translate into weaker capital formation. Total deep tech funding in Southeast Asia rose 19% year-on-year to $999.2 million in 2025.

The report argues that this divergence points to a market where capital is still being deployed, but with greater discipline. Investors are making fewer broad-based bets and concentrating funding in higher-conviction companies with clearer technical moats, stronger IP defensibility, proven commercial demand and more visible paths to category leadership.

Capital is still being deployed, but with greater discipline.

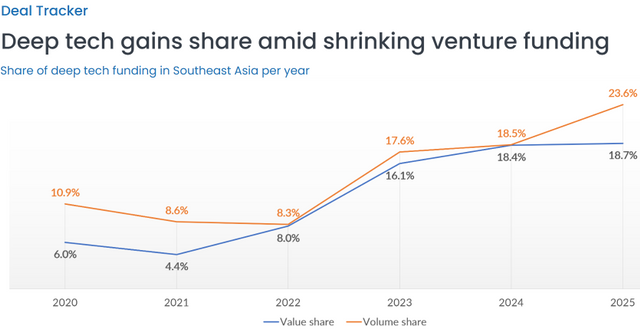

Deep tech’s relative position also strengthened within Southeast Asia’s broader venture market. The segment accounted for 23.6% of total venture-backed deal volume in 2025, up from 18.5% in 2024 and more than double its share in 2020, reinforcing the view that deep tech is becoming more consequential even as the wider funding market remains under pressure.

The sharper rise in volume share suggests that deep tech is gaining relevance across the funding pipeline, rather than being lifted only by a handful of large rounds. Investors appear to be widening their exposure to IP-led and technically differentiated startups, but are still prioritising commercialisation pathways, capital-efficient scaling and evidence of defensibility over broad sector exposure.

Early-stage gravity

Deep tech funding in Southeast Asia remained overwhelmingly early-stage in 2025, with 103 early-stage deals accounting for 94.5% of total volume. The report argues that this reflects a market still largely in company-building mode, with most activity concentrated from seed to Series B and relatively few startups ready for growth-stage capital.

Most deal activity is concentrated from seed to Series B stages.

The increase in late-stage activity, however, is encouraging. Late-stage deal volume rose to six transactions in 2025 from just two in 2024, while late-stage funding value climbed to $343 million, or 34.3% of total deep tech capital raised.

The larger late-stage rounds were led by companies such as Ultragreen.ai, Singauto and BECIS. Their ability to attract sizeable cheques suggests that more technically differentiated startups are beginning to clear the commercialisation and scale-up hurdles required to access growth capital.

Even so, the market remains narrow. Early-stage funding still dominated at $656 million, underscoring that late-stage depth remains dependent on a small pool of breakout companies rather than a broad base of scale-ready deep tech startups.

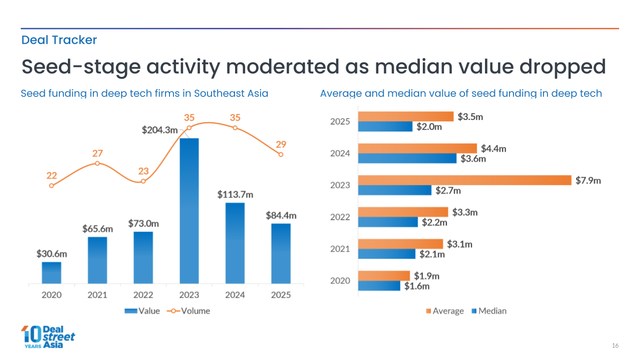

At seed stage, round sizes moderated. The median seed round fell to $2 million in 2025 from $3.6 million in 2024, while the average declined to $3.5 million from $4.4 million. This points to more disciplined entry pricing and tighter capital deployment at company formation, as investors become more selective around technical validation, founder capability and the path from R&D to early commercial traction.

Series A showed a more uneven pattern. The median round size eased to $8.5 million from $10.5 million, but the average rose to $17.1 million, suggesting that capital was concentrated in a smaller number of larger rounds rather than distributed more evenly across the Series A pipeline.

Deep tech undervalued

Fund managers and founders interviewed for the report see Southeast Asia’s deep tech opportunity moving from niche promise to strategic relevance, as the region becomes more important to global technology supply chains, scientific talent formation and innovation-led industrial development.

Vertex Ventures Managing Partner Chua Joo Hock argues that deep tech in Southeast Asia remains meaningfully undervalued, with semiconductors and related supply-chain plays standing out as especially compelling. He points to the China+1 shift and how it is creating a strong pipeline of opportunities across Singapore, Malaysia and the broader region.

The China+1 shift is creating a strong pipeline of opportunities across Singapore, Malaysia and the broader region.

“The semiconductor ecosystem here is more developed than most people realise, government support is robust, and international customers are actively looking to diversify. Together, these tailwinds are attracting serious founders building the next generation of deep tech in the region,” said Hock.

The funding backdrop, however, remains demanding. Dr Michael Fehlings, Co-founder and CEO/CTO of ImmunoScape, says the global funding environment is still challenging, particularly for early-stage biotech companies.

“For companies developing advanced cell therapies, the bar has increased significantly. Investors want to see not only compelling biology but also a credible strategy to address some of the historical challenges of the field, including manufacturing complexity, scalability, durability of response, and cost of goods,” said Fehlings.

For ImmunoScape, he said the strategy has always been to combine the strengths of multiple ecosystems, with Southeast Asia serving as a strong base for scientific talent and institutional support, while North America remains critical for specialised biotech capital, clinical development and strategic partnerships.

Focus on health and green tech

Health tech and green tech were the most active deep tech verticals in Southeast Asia in 2025, with 21 deals each, the report finds. They were followed by Software & IT with 15 deals and Data analytics/AI/ML with 10, underscoring where investor appetite is clustering within the region’s deep tech pipeline.

The pattern suggests that capital is gravitating towards sectors where proprietary innovation can address large, structural demand. In healthcare, this includes diagnostics, therapeutics, medical devices and delivery models. In green tech, it reflects demand for climate transition, energy efficiency, waste management and industrial decarbonisation solutions.

By funding value, health tech was the clear leader, attracting $369 million in 2025, according to the report. That put it well ahead of green tech at $144 million and Data analytics/AI/ML at $123 million, suggesting that the healthcare opportunity set produced more capital-intensive and potentially later-stage funding rounds.

Green tech and AI, by contrast, remained thematically strong, but funding was more uneven across companies and sub-segments, the report finds. While both verticals continue to benefit from strong thematic tailwinds, investor deployment appears more selective, with capital directed towards companies that can show clearer technical differentiation, enterprise demand or infrastructure relevance.

Software & IT’s relatively high deal volume but lower funding value, at $43 million, points to a wider base of smaller or earlier-stage transactions, driven largely by blockchain-focused startups, the report notes. Overall, the data points to a deep tech market where capital is clustering around sectors with clearer technical moats, commercial urgency and more credible routes to scale.

AI as a deep tech layer

AI is also emerging as a more important layer in Southeast Asia’s deep tech stack, not only as a standalone category but as an enabler of more defensible technology businesses across hardware, infrastructure and enterprise software.

Elev8.vc Managing Director Adithya Mathur expects AI to become foundational to deep tech over the next 12 to 24 months. He sees three areas shaping the firm’s investment focus: high-compute infrastructure, frontier AI applications, and edge AI or cyber-physical systems.

“The biggest shift will be from experimentation to deployment. Enterprises are increasingly moving beyond proofs of concept and demanding solutions that deliver measurable operational outcomes,” Mathur said, while adding that successful startups will be those that combine AI capabilities with proprietary data, domain expertise and deep integration into customer workflows

Separately, Adrian Hia, a partner at Kairous Capital, said the opportunity is not AI in the abstract, but what AI now makes possible in markets where digitisation has historically been too costly, fragmented or operationally complex.

This includes lower-cost digitisation for under-digitised industries and more accessible tools for the long tail of B2B customers that were previously difficult to serve. For the region’s deep tech ecosystem, the report suggests, AI’s relevance may lie less in generic application-layer plays and more in its ability to unlock new commercial pathways for technically differentiated companies.

“Over the next 12 to 24 months, we expect a wave of researchers and operators who understand Southeast Asia’s problems deeply to start building deep tech solutions that are genuinely suitable for the local market with the help of AI,” Hia said.

The Southeast Asia Deep Tech Review: 2025 report has extensive data on:

- The number of venture deals sealed and funds raised by deep tech startups in SE Asia since 2020.

- The most funded SE Asian deep tech startups of 2025

- Fundraising trends by deep tech category

- Fundraising trends by country

- Early- and late-stage fundraising trends

- Insights from industry experts